VCM spot volume experienced an uptick last week, largely due to acquisitions from Australian firms gearing up for end-of-month and annual reporting obligations, according to Xpansiv data. These purchases contributed to a total CBL spot VCM volume of 394,632 metric tons, a notable increase from the previous week’s tally of just under 120,000.

Xpansiv provides robust market data from CBL, the world’s largest spot environmental commodity exchange. These include daily and historical bids, offers, and transaction data for various environmental commodities traded on the CBL platform.

Xpansiv’s VCM Spot Volume

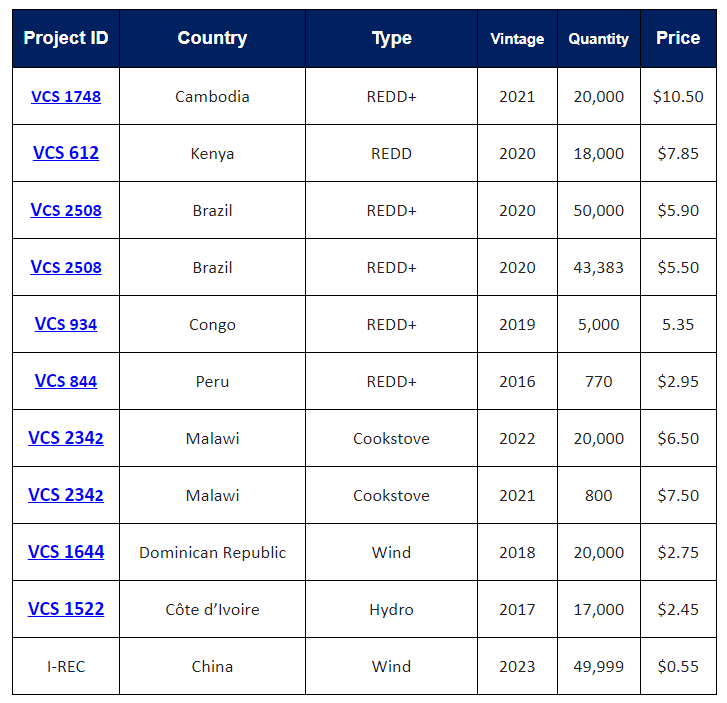

The bulk of trading activity for the week centered around over-the-counter (OTC) blocks of Latin American nature credits. Newer-vintage REDD+ credits commanded prices as high as $7.50 per ton, while older vintage AFOLU credits were observed crossing at $0.37.

Notably, vintage-specific mispricings were observed in the Katingan and Rimba Raya project credits. The older vintages are trading at premiums compared to newer ones.

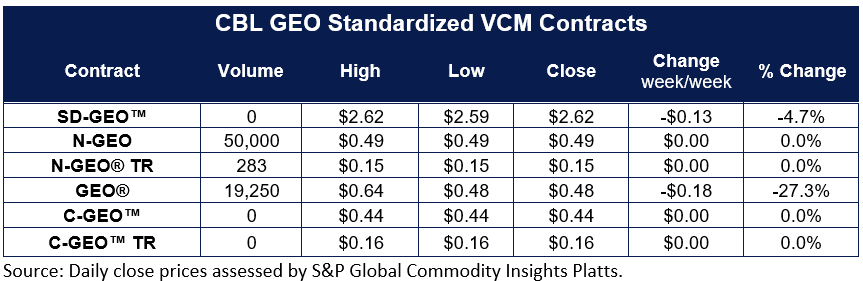

Meanwhile, CBL GEO prices saw a significant decline of over 20%. The pilot-phase CORSIA bellwether spot and December futures contracts closed at $0.48 and $0.38, respectively.

Last Thursday witnessed the bulk of trading activity, with 1,612,000 tons exchanged, including 1,462,000 Dec 2024-2025 calendar spreads priced between -$0.16 and -$0.19.

Amidst a backdrop of cautious optimism, market participants in Europe discussed progress with various initiatives such as ICVCM, VCMI, ICAO, and SBTi. However, there remained uncertainty regarding the timing of increased corporate VCM participation, with discussions revolving around the theme of “Survive to 2025”.

In terms of new listings, REDD+ project credits dominated, with carbon prices ranging between $10.50 and $2.95. Notable offerings included 20,000 Cambodia vintage 2021 REDD+ credits and nearly 95,000 split vintage Brazilian REDD+.

Additionally, 45,000 China hydro vintage 2023 I-RECs were listed at $0.55.

RECord Breaker: Xpansiv Sets New Standards in Renewable Energy Trading

At a renewable energy event in Amsterdam, CBL announced record Renewable Energy Credits (REC) volumes in Q1, signaling bullish sentiment in the market.

REC volume on its CBL spot exchange set a record of 494,249 MWh in Q1 2024. A record 61,600 California Low Carbon Fuel Standard contracts were also traded on the spot exchange.

Remarking on this achievement, Ben Stuart, Chief Commercial Officer, Xpansiv, noted that:

“Growth of our compliance REC business continues to demonstrate the utility of Xpansiv infrastructure to the US renewables markets. Our strong position as the platform of choice for corporates seeking products to satisfy reporting obligations and net-zero commitments continues to make Xpansiv an essential partner for the global energy transition

In the North American compliance market, NEPOOL RECs resumed trading on CBL, with over 62,000 credits exchanged for Q4 2023 generation. Rhode Island new generation credits led in volume, followed by 2023 Massachusetts class 1 and solar 2 credits.

In PJM markets, Maryland 2024 class 1 credits and Ohio solar credits were actively traded. Lastly, over 80,000 NAR credits were exchanged via CBL, consisting primarily of 2023 US-sited wind credits with some CRS eligibility.