India’s bold move in 2024 to revamp its Carbon Credit Trading Scheme (CCTS) marks a significant step forward in the country’s efforts to combat climate change. This revision allows non-obligated entities, including companies and individuals, to actively participate in the tradable carbon credits market. By opening up this market to voluntary players, India is providing an avenue for entities to take proactive steps in reducing their carbon footprint and addressing planet-warming emissions.

Under this revamped scheme, companies and individuals now have the opportunity to voluntarily invest in carbon credits as a means to offset their own emissions. Carbon credits represent a quantifiable unit of carbon dioxide or other greenhouse gases that are either reduced or removed from the atmosphere through various initiatives such as renewable energy projects, reforestation efforts, or energy efficiency improvements. By purchasing carbon credits, participants effectively contribute to these projects, thereby compensating for their own emissions and supporting climate action initiatives.

The inclusion of non-obligated entities in the carbon credit trading market signifies a broader recognition of the importance of collective action in addressing climate change. By empowering companies and individuals to voluntarily engage in carbon offsetting, India is fostering a culture of environmental responsibility and sustainability within its society. This move not only aligns with global efforts to mitigate climate change but also reflects India’s commitment to promoting environmental stewardship and sustainable development.

Moreover, the revamped CCTS has the potential to stimulate economic growth and innovation by incentivizing investments in green technologies and projects. As more companies and individuals participate in the carbon credits market, there is an increased demand for sustainable solutions, driving investment in renewable energy, carbon sequestration, and other climate-friendly initiatives. This, in turn, can create new business opportunities, generate green jobs, and foster the transition towards a low-carbon economy.

This significant revision introduces an offset mechanism, enabling these entities to register projects and obtain tradable carbon credit certificates (CCCs). Each credit represents one tonne of carbon dioxide equivalent (tCO2e). The aim is to efficiently price emissions through CCC trading and expand the voluntary carbon market.

India Opens Doors for Voluntary Carbon Credit Buyers

In 2023, India introduced the 2023 Carbon Credit Trading Scheme (CCTS), encompassing both compliance and voluntary sectors. However, while the compliance segment is scheduled to commence in 2025-26, there is no set timeline for the launch of the voluntary carbon market.

Under India’s revised carbon market scheme, obligated entities have the flexibility to purchase additional credits or sell surplus ones. Meanwhile, businesses can trade CCCs to offset their emissions.

However, sectors facing challenges in meeting reduction targets, particularly those with hard-to-abate emissions, are exploring the possibility of trading energy-saving certificates (ESCerts) and renewable energy certificates (RECs) as offsets.

India emerged as a favorable destination for energy transition investments after successfully hosting the G20 Summit last year. During the same year, the country added about 17 GW of capacity, with non-fossil additions accounting for 13.8 GW.

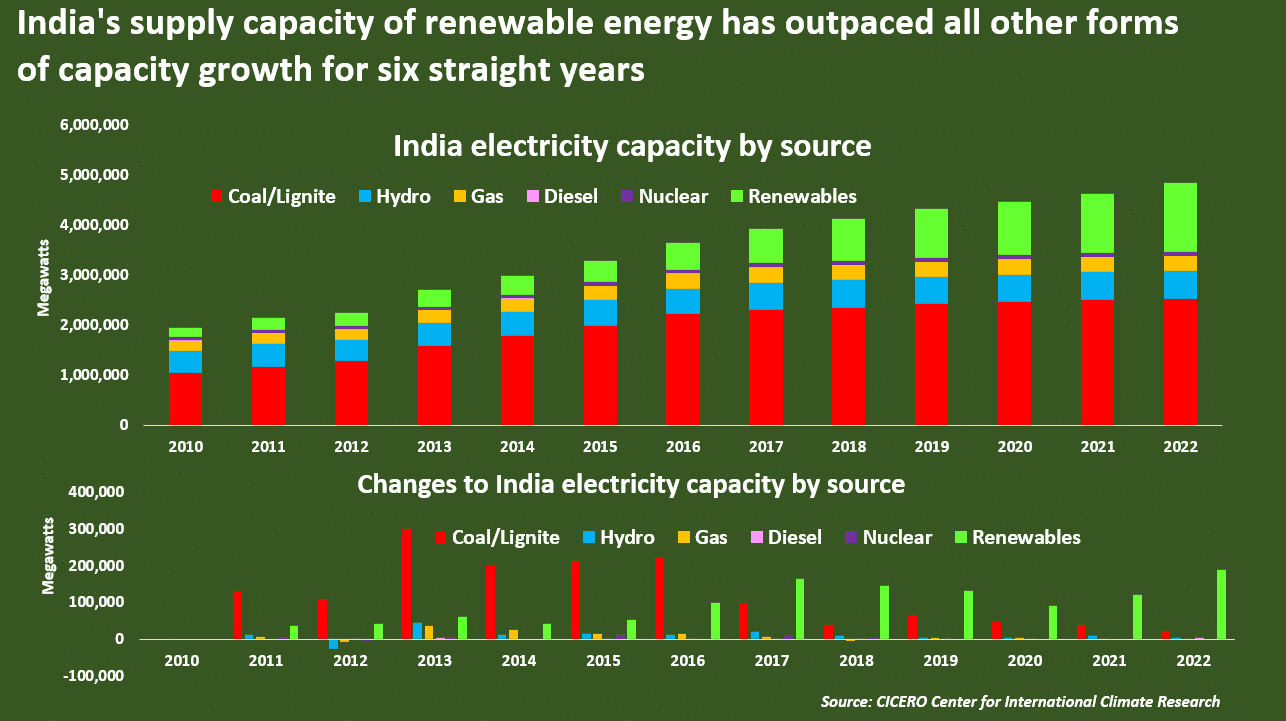

As seen below, renewable energy has the largest growth in terms of electricity supply capacity in the South Asian country.

Moreover, India increased its financial support to propel the green hydrogen ecosystem and initiated preparations for its domestic carbon markets.

Key decisions regarding international participation in the carbon credit market are expected in 2024, setting the trajectory for India’s engagement. Additionally, discussions on the scope, design, and procedures of the scheme, including linkages with international standards and registries, are anticipated to be addressed.

India’s Energy Transition Priorities to Drive Climate Action

India’s move reflects its commitment to combating climate change and aligning with global efforts towards decarbonization. This year, the super-emitter is anticipated to intensify its efforts in implementing its energy transition strategy while navigating challenges related to energy security and affordability.

India’s strategy will prioritize various aspects in power and renewables market, including:

Clean energy transition advancing; coal reliance to remain high:

- Electricity demand to grow with GDP growth, driven by local activity due to elections and El-nino impact.

- Total capacity addition to grow by 60% YoY; coal share in generation to decrease marginally to 73.2% in 2024.

Improving domestic fuel supply (Coal and Gas) remains top priority:

- India expected to surpass 1 billion metric tons of domestic coal production in 2024.

- Boost in domestic gas production due to new gas pricing reforms.

Focus on green hydrogen/ammonia:

- Shift towards creating local demand and supporting excess costs.

- Launch of new schemes to aggregate demand from public sector units and large consumers.

Renewables at the forefront of India’s climate policy:

- Highest renewable capacity addition (>20 GW) expected in 2024.

- Falling module costs and tender backlog driving record capacity addition.

- Increasing prominence of hybrid renewable tenders and stand-alone storage tenders.

Bridging the Gap: Integrity Measures and Global Carbon Markets

The strategy also underscores the importance of integrity measures in bridging the emissions reduction gap and achieving climate goals.

In a recent report by the Carbon Market Institute, global carbon pricing mechanisms have raised an impressive $100 billion in 2022 and now covered 23% of global greenhouse gas emissions.

Despite these achievements, current government pledges are projected to result in a temperature rise between 2.1°C and 2.8°C. Carbon markets hold considerable potential to bridge the emissions reduction gap necessary to approach a 1.5°C trajectory.

However, there is still work to be done to bolster integrity measures and accelerate international cooperation in this regard.

In 2023, the global carbon trading markets experienced robust growth, reaching a record value of over $947 billion, representing a 2% increase from the previous year. This growth was primarily driven by higher prices in key markets such as Europe and North America, despite similar permit trading volumes.

The EU’s Emissions Trading System (ETS) maintained its position as the most valuable market, accounting for 87% of the global total. However, weakening demand from industrial buyers and the power sector towards the end of 2023 led to a bearish trend that has persisted into 2024.

Conversely, North American prices reached record highs, and China’s national ETS also saw unprecedented price levels in 2023.

India’s revised Carbon Credit Trading Scheme (CCTS) presents a significant step forward in the global effort towards decarbonization. This, combined with the strong growth observed in the global carbon trading market, underscores a promising trajectory towards reducing greenhouse gas emissions.